The Better Way Alliance Proposes Federal Commercial Mortgage Support

From cafes to hardware stores, Canada’s rich history of small business ownership has kept neighbourhoods vibrant for decades. Over that time, business owners retired and sold their properties – often to large landholding companies. Now Canada’s main streets are facing a distressing situation where few business owners actually own their spaces.

Compared to 3 decades ago, far less commercial real estate is held by small-time business owners. This is troubling for 3 big reasons:

- There are no protections for commercial rent increases. Landlords can increase rent by any amount at the end of a contract – and sometimes in the middle of one (read our blog on triple-net-leases).

- Businesses have no certainty that they may continue operating in the space at the end of their lease. Even long-time businesses can be evicted for no reason.

- A disproportionate amount of power is held by landlords during any disputes or even simple lease negotiations.

While many businesses may not want the headache of land ownership, some experienced business owners are leaning toward purchasing property as a way to stabilize their business and ensure its continued operation.

However, accessing a commercial mortgage as a business owner is difficult and for many, impossible. Banks won’t take any risk – even for experienced and long-time businesses. If they do, they’ll often require 50% down or more. Private lenders might offer a mortgage but the interest rates tend to be astronomical with predatory terms.

For businesses that want to own their building, there are few options short of a jackpot inheritance or selling their family home.

Businesses Facing Major Rent Increases Have Few Options

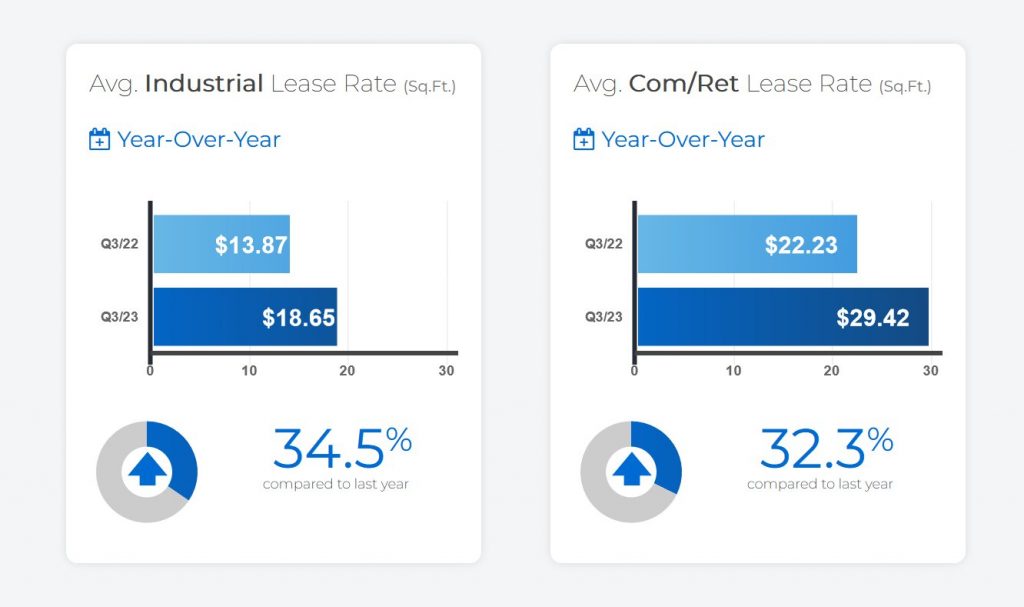

In recent years, commercial rent has skyrocketed – over 30% in Toronto from 2022-23. This is pushing more smaller businesses out of their spaces while leaving main streets affordable only to chains and luxury retailers.

Image: TRREB Toronto 2022-23 Q3 Snapshot comparison (taken February 15, 2023).

Heightened lease costs combined with lack of access to commercial mortgages for small business owners has sent many businesses into insolvency. The double whammy of increased rents and operating costs has led many to cease operation or go bankrupt.

When a business is facing a large rent increase, there are three options:

- Agree to it and try to increase revenue to pay for the increase

- Find another location

- Close the business

Business closures because of rent increases are common – but any of these outcomes cause a major disruption to the business. In the case of East India Pantry in Mississauga, they were forced to vacate their retail space of 40 years after a 300% rent increase. They found a new warehouse space which has allowed their wholesale to flourish but their iconic retail store has yet to come back. Had they owned their space, they’d still be operating their retail store while scaling the wholesale business.

Improved Access to Business Owner Mortgages = More Stability

The Better Way Alliance’s solution is a Federal commercial mortgage support program via the Business Development Bank of Canada (BDC). The BDC would act as a mortgage guarantor, supporting qualified brick-and-mortar businesses in their quest for sustainable growth and stability.

Our proposal achieves this while improving the stability of neighbourhoods by investing in already successful local business leaders. Keeping ownership local also keeps these businesses tapped into ther local communities.

Property ownership for businesses means more than just a place to operate; it creates lasting community wealth and ensures the vibrance of local neighbourhoods. The shift towards fewer small business owners holding real estate calls for action. For example, in New York City, the majority of commercial landlords own 5 or more properties – a trend likely mirrored in Canada.

In 2017, Garab Serdok’s decision to sell his home to buy a building post-rent increase demonstrates the extreme measures business owners must consider. The proposed BDC program offers a less drastic solution.

Rationale for Government Intervention

Government support in the form of a Federal Commercial Mortgage Program would help people like Garab Serdok purchase their buildings without putting their life savings at risk or needing to sell their house. Businesses with proven sales over a minimum period of time, positive cash flow, and stability could apply for a BDC led commercial mortgage guarantor program.

Acting as a guarantor for commercial mortgages, the BDC would reduce the financial risk for lenders, making it more feasible for small businesses to secure the loans they need to purchase property.

Canada’s commercial rent market is wildly unpredictable. Leveling the commercial real estate playing field will allow more local businesses to stay in the communities they love – and potentially help keep rent from increasing quickly over short periods of time.

Benefits of a Federal Commercial Mortgage Program

Small businesses can establish a stable foundation for growth through property ownership. When residents move to a new neighbourhood, often it’s because of the small businesses and amenities they have access to. Residential real estate agents often highlight these local businesses in brochures.

Yet, over time, many of these businesses are pushed out of neighbourhoods by quickly rising rents and replaced by chain stores.

There are many benefits to keeping our main streets local:

- Stability and Growth: Owning commercial property provides businesses with a sense of stability, freeing them from the uncertainties of leasing and allowing for long-term planning and investment in growth and good jobs.

- Economic Resilience: Property ownership can act as a financial asset for small businesses, offering a buffer against economic downturns and enhancing the overall resilience of the Canadian economy – while avoiding potential layoffs.

- Community Development: Small businesses that own their properties are often able to invest more in their local communities, contributing to the vibrancy and health of main streets across the country.

Why BDC is the Right Vehicle for Change: The Business Development Bank of Canada, with its mandate to support small and medium-sized enterprises, is perfectly positioned to administer this program.

BDC’s existing infrastructure and expertise in business financing can ensure the program’s efficient and effective implementation. Moreover, BDC’s willingness to embrace more risk and support underserved and equity-seeking communities is a right-place, right-time moment for a mortgage guarantor program.

The Path Forward: The creation of a Federal commercial mortgage support program through BDC represents a step toward a more inclusive and prosperous economy. By addressing the critical challenge of property ownership for small businesses, the government can catalyze a wave of entrepreneurial energy.

The current wave of business bankruptcies and insolvencies highlights the need for stronger main street supports. Embracing commercial property ownership by small business owners has a multitude of benefits. The Better Way Alliance urges the Canadian government to adopt this policy idea and develop a program that supports Canada’s small businesses and main street resilience.

Recent Comments